- 08.06.2026.

- News, Management

In 2026, Croatia has a larger charter fleet than Greece, but lower rental prices and weaker occupancy. The analysis shows that Greek charter companies generate higher revenue per vessel, extend the season further and hold prices more successfully outside the summer peak. Charter market analysis based on yacht-rent.com and eVisitor April 2026/DZS data, June 2026.

According to data aggregated on the Croatian portal yacht-rent.com, Croatia has 3,761 charter vessels available, while Greece has 2,542. The average weekly price of a sailing yacht in Croatia is €2,753, compared to €3,425 in Greece. The average annual occupancy rate of a sailing yacht in Croatia is 32.5 per cent, versus 43.6 per cent in Greece.

The pattern is consistent across all three vessel categories: sailing yachts, catamarans and motor yachts. Croatia's charter industry operates a larger fleet yet generates lower revenue per vessel than its closest Mediterranean competitor. This analysis does not answer why, it shows what.

Market Context: What Is Happening Around the Charter Sector

Nautical tourism is part of a broader picture. According to eVisitor data, in the first ten months of 2025 Croatia recorded 20.9 million arrivals and 107.9 million overnight stays, representing year-on-year growth of 2.3 per cent in arrivals and 1.2 per cent in overnight stays. The Adriatic coast continues to account for 88 per cent of total tourist traffic.

The pre-season figures for 2026 are more relevant to the charter sector. In the first quarter, January through March, arrivals rose by 9.4 per cent and overnight stays by 8.5 per cent compared to the same period in 2025. Austria recorded arrival growth of 32 per cent, Germany 37 per cent. These two countries form the backbone of the European sailing market and typically book early in the season. That early demand is reflected in the charter occupancy data.

On the cost side, according to the Croatian Bureau of Statistics, the number of vessels in transit at Croatian nautical marinas fell by 3.8 per cent in 2024 compared to 2023, marking the second consecutive annual decline. At the same time, marina revenues reached €180 million, an increase of 12.1 per cent. Fewer vessels, higher marina revenues — berth fees are rising faster than traffic. That is a cost charter operators cannot ignore, and one that does not appear in vessel rental data.

The inflation rate for tourism services in Croatia stands at 7.9 per cent year-on-year as of May 2026, according to DZS data. Overall HICP inflation is 4.9 per cent, the third highest in the eurozone. A guest arriving from Austria or Germany is paying more for every element of their stay — charter rental, berth fees, fuel, food and drink. How far that pressure is influencing booking decisions and destination choice is something the charter industry can, for now, only estimate.

What the Charter Supply Data Shows

The analysis is based on yacht-rent.com data for 2026, covering 3,761 vessels in Croatia and 2,542 in Greece, broken down by vessel type and number of cabins. The data includes average prices, price ranges and booking occupancy rates. Industry estimates suggest the total Croatian charter fleet numbers around 4,500 vessels, meaning the yacht-rent.com sample covers approximately 84 per cent of the market. The methodology is consistent across both destinations and the same year, making the figures directly comparable.

Sailing Yachts: The Largest Segment, the Largest Gap

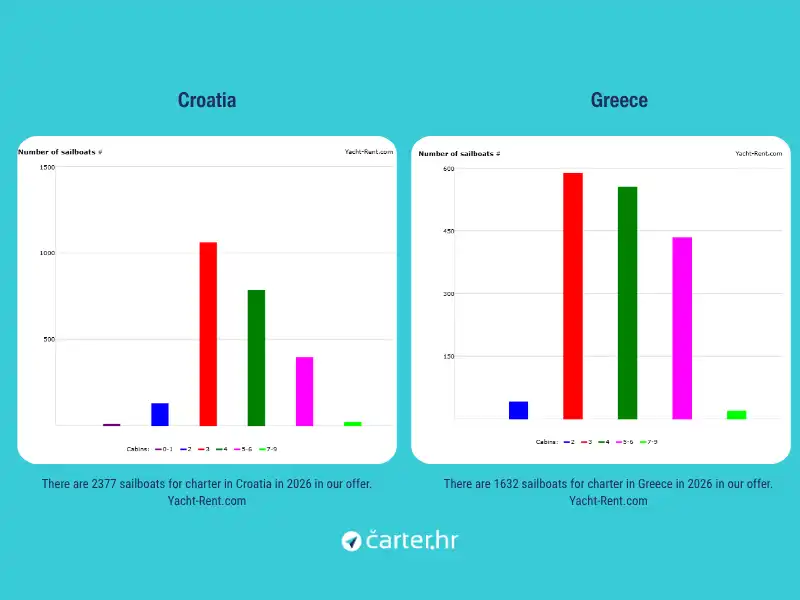

Sailing yachts are by far the largest category. Croatia has 2,377, Greece 1,632. Greek sailing yachts achieve on average 24 per cent higher weekly prices (€3,425 versus €2,753) and 11 percentage points higher annual occupancy (43.6 per cent versus 32.5 per cent).

One notable feature of this season: peak occupancy for Croatian sailing yachts was recorded in the week of 30 May, at 88.4 per cent. For Greek sailing yachts, peak falls in mid-September at 82.2 per cent. Such an early-season peak has not been recorded for Croatia in the available data from previous seasons, and it is unlikely to be coincidental. eVisitor data for January to March 2026 shows arrivals from Austria up 32 per cent and from Germany up 37 per cent compared to the same period in 2025. Both are leading charter markets that book in advance and tend to arrive at the start of the season. That booking pattern is likely one of the factors that shifted Croatian demand towards the first half of the season, though without access to the internal booking systems of charter companies no definitive conclusion is possible.

The seasonal price range for sailing yachts runs from €2,137 per week (average 3-cabin vessel in-season) to €6,926 (peak 5-6 cabin). In Greece, comparable categories are 15 to 30 per cent more expensive, with a smaller drop towards the end of the season.

Catamarans: Almost the Same Fleet, a Different Price

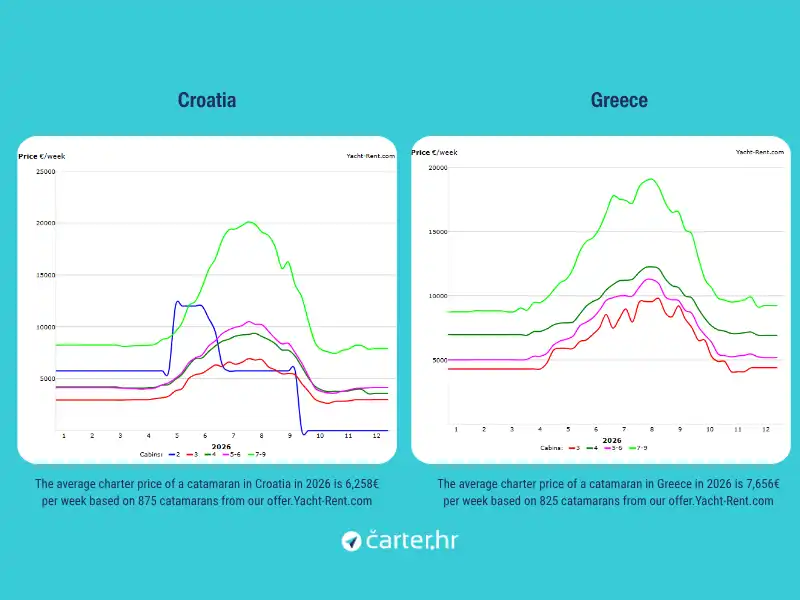

Croatia has 875 catamarans, Greece 850. The difference in fleet size is negligible. The difference in price and occupancy is not. Greek catamarans achieve an average of €7,586 per week versus €6,258 in Croatia, a gap of 21 per cent. Annual occupancy: Greece 42.6 per cent, Croatia 35.4 per cent.

Croatia records a price drop of 64 per cent between the peak week (25 July, €11,199 for a 5-6 cabin catamaran) and late October (€3,988). In Greece that drop is 54 per cent. Greek charter companies discount less outside peak season — and succeed in holding those prices.

Motor Yachts: High Price, Low Occupancy

Motor yachts are a specific case. Croatia has 509 motor yachts in the sample; Greece has just 60, too small a number for a reliable cross-country comparison. The average weekly price in Croatia is €12,788, with annual occupancy of 15 per cent, roughly eight weeks of active use per year. Peak occupancy does not exceed 47.9 per cent even in July. This is the most expensive and least occupied segment.

A note on costs: this analysis does not cover marina berth fees and winter lay-up costs for the charter fleet. These vary from marina to marina and are not available in structured form for the market as a whole. They are particularly relevant for motor yachts, where fixed costs per vessel — berth, maintenance, insurance — are disproportionately high relative to the number of weeks billed. Marina revenues rose 12.1 per cent in 2024, according to DZS, which means that cost has not been standing still.

What Greece Does Differently

The data does not say why the gap exists. It says the gap exists and how large it is. Several patterns are nonetheless consistent enough to be difficult to ignore.

The Greek season is longer. Peak for sailing yachts falls in September, not May or July. Demand is more evenly distributed across the season, which reduces pressure to discount in the shoulder months. Greek charter companies achieve a premium outside July and August. Croatia's fleet is 48 per cent larger than Greece's, without a proportionally larger demand across all segments. Greater supply against limited demand typically pushes prices downward — and that effect is visible in every segment.

There is also the question of price positioning. In public discourse, Croatia is often perceived as an expensive destination, particularly in the hotel and restaurant sector. Charter data suggests the opposite: in every segment, Greece is more expensive and better occupied. Why that is the case is not visible in the available data, but the question deserves attention from charter operators thinking about their own positioning.

The Question That Remains Open

The Adriatic is one of the most attractive nautical destinations in the world. The 2026 data suggests that position is not being monetised at the level the size of the fleet and the quality of the destination would imply.

A season that ends in September is worth less than one that runs to November. A vessel going into winter lay-up in October costs more than one still operating in October. A fleet competing primarily on price builds a premium position slowly. Marina costs are rising faster than rental revenues, at least according to the 2024 data.

Whether these patterns will change, and what would be required for that to happen, is a question for charter operators, for marketing, and for broader industry discussion. The numbers are there. Each operator draws their own conclusions, based on their own situation and their own data.

Methodological Notes and Sources

Charter supply and pricing: yacht-rent.com, updated May and June 2026. Croatia: 3,761 vessels (sailing yachts 2,377, catamarans 875, motor yachts 509). Greece: 2,542 vessels (sailing yachts 1,632, catamarans 850, motor yachts 60 — sample too small for reliable comparison with Croatia). Occupancy is measured on vessels with booking calendars updated within the previous seven days, which is a subset of the total sample. Annual occupancy figures include off-season weeks.

Tourist traffic: eVisitor / Ministry of Tourism and Sport of the Republic of Croatia, cumulative data for January to October 2025 and January to March 2026.

Nautical marinas: Croatian Bureau of Statistics, TUR-2024-2-1 Nautical Tourism, capacities and operations of nautical tourism ports in 2024, published May 2025.

Inflation: Croatian Bureau of Statistics and Eurostat, HICP data for May 2026.

This analysis does not include marina berth fees, winter lay-up costs or vessel maintenance for the charter fleet. This data is not publicly available in structured form for the market as a whole.

Charts and interactive dashboard available at yacht-rent.com

Categories of trends

- News

- Sale

- Marketing

- SEO

- Web design

- Social media

- Technology

- Regulations

- Management

- Education

- Finances

- User experience

- Graphic design

Newsletter

Sign up for the newsletter and receive the latest trends and tips straight to your inbox