When we analyse the economic picture of Croatia after its growth in real GDP by around 2.3% in 2023, the question arises: What awaits us in 2024? Ivica Žuro provides a deeper insight into economic forecasts that define expected growth, slowing inflation, changes in the labour market, and the impact of monetary policy on interest rates.

After the real GDP of Croatia grew by approx. 2.3% in 2023, what can be expected in 2024?

Growth of 2.5% is the determinant of the forecasts of all domestic bank macroeconomists. The prophets (a joke, of course) or the European Commission macroeconomic analysts agree with them. At the same time, the Croatian National Bank expects growth of an easily possible 3%.

Predictions - wage growth and inflation decline?

These expectations are based on faster growth in actual personal consumption - 3.1% in 2024 versus 2.4% in 2023.

Inflation is also expected to slow down to 3.6%, which will remain above the EU average due to domestic production growth.

The continued growth of the average salary at a rate of 8.6% is also something that should not be surprising.

Although investment growth is forecast to be slower - 2.2% in 2024 versus 3.8% in 2023 - a gradual recovery of economies in Central Europe is expected, led by a slight recovery in Germany, so that exports could grow at a rate of 3.4% and imports at a slightly higher rate of 3.9%.

With such developments, the unemployment rate could fall to 6.2%.

In accordance with the government's plan, a budget deficit of up to around 2% of GDP is expected, which should keep the ratio of external debt in relation to GDP above the 60% mark.

The impact of monetary policy and changes in interest rates

During the second half of 2023, the effects of the tightening of the European Central Bank's monetary policy continued to spill over into the financing costs of companies and households in domestic banks.

To put it in specific terms - with the stroke of a pen, the interest on our loans was raised.

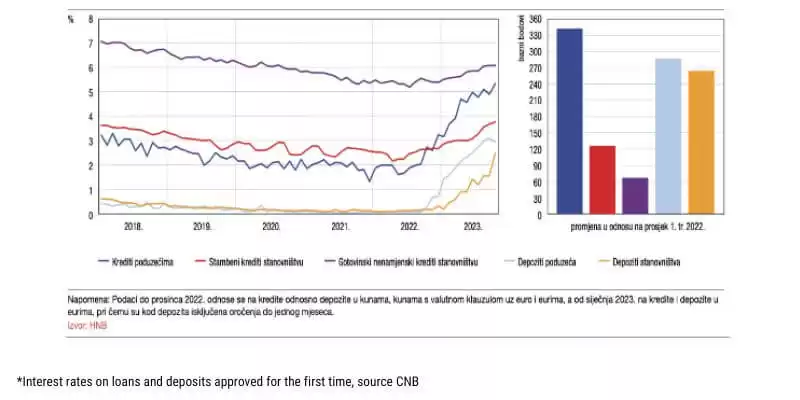

The average interest rate on loans contracted for the first time to non-financial companies reached an average of 5.3% in IX 2023, or 36 basis points more than in June of this year.

The cost of financing the population also increased. The average interest rate on housing loans contracted for the first time in October was 3.8% and 6.1% for non-purpose cash loans, which is 68 and 23 basis points higher, respectively, compared to the average level in June of the current year.

The increase in the interest rate on housing loans partly reflects the termination of the effect of the state program of subsidizing housing loans with a more favourable interest rate - translated: the incentive housing program has gone to eternal hunting grounds.

The tightening of financing conditions compared to the first part of 2022 was recorded for companies that borrowed at a 338 basis points higher interest rate in October and households at 126 basis points for housing and 67 basis points for non-purpose cash loans.

Interest rates on loans and deposits

And interest rates on term deposits continue to rise, especially on household deposits.

Thus, the average interest rate on the first-time deposits of households in X 2023 reached 2.5%, which was 107 basis points more than in June of this year, while in the same period for companies, the increase amounted to 45 basis points with an interest rate of 2.9%.

Parallel to the increase in interest rates on new businesses, interest rates on existing loans and deposits also increased.

The growth of interest rates on existing loans to companies was particularly pronounced due to the increase in interest rates at which new loans are granted.

This is mainly due to the representation of EURIBOR as a reference parameter in loans contracted with variable interest rates.

53% of company loans are contracted with variable interest rates, and 75% of these loans are linked to EURIBOR.

The increase in interest rates on existing loans to households is limited and delayed by the longer average maturity of loans, which reduces the contribution of the increase in interest rates on new loans and the significant presence of interest rates that are fixed at least for a certain period.

46% have an agreed fixed interest rate during a specific period or even until maturity.

Another factor preventing higher growth is the nomination of the national reference rate (NRR) among the reference parameters, with a share of around 68% in household loans.

Again, the letter of the law influenced the retention of interest rates: the maximum variable interest rate is limited by the Law on Consumer Credit and amounted to 3.79% for the last period.

If not - they would have a new case of CHF.

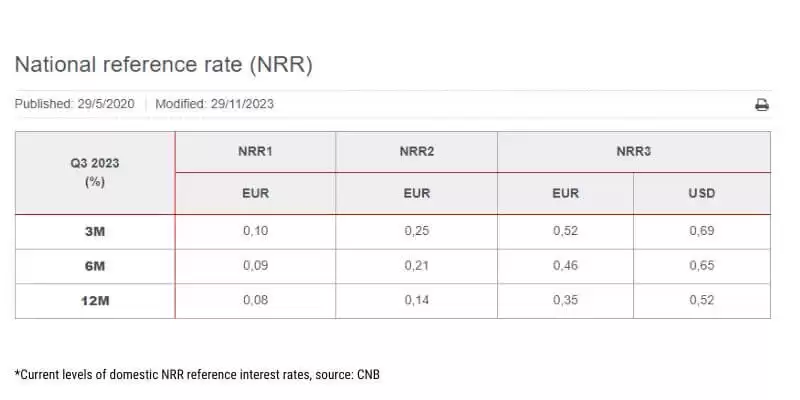

Understanding the National Reference Rate (NRR)

And as far as the NRR is concerned, it should also increase because it refers to citizens' deposits with domestic banks.

This particularly means - while the interest on deposits was outrageously low - the volume of savings and the cost of interest on deposits were also down. And in the end, the amount of the total interest rate of the NRR, even in the basic version, was low.

The last time it was announced a month ago, the prevailing euro NRR1 applied to citizens was increased only minimally, from 0.06 to 0.1%. Still, it could be much more noticeable during the subsequent announcements in February and May 2024.

And what are we talking about here anyway?

NRR is the average cost rate of sources of funds in the Croatian banking sector (banks, savings banks and branches of foreign banks) concerning:

- certain past reference period (3, 6 or 12 months),

- type of source (deposits of natural persons, deposits of legal entities from the non-financial sector, all other sources of bank funds) and

- relevant currency (euro and US dollar).

So, if somewhere in the interest rate, it is stated that it amounts to 3M NRR1 + 4.0 pp (percentage points or points) - at the present moment, according to the value in the table above, this value is 4.10% (0.10% + 4, 0).

For the purpose of calculating the NRR, the CNB calculates indicators of interest costs of the Croatian banking sector for the main sources of funds during the previous quarter, as well as indicators of the state of these sources of funds at the end of each month of the calculation quarter to which the said interest costs refer.

Indicators are calculated based on data from non-consolidated interim reports for banks, that is, monthly and quarterly data that banks submit to the domestic central bank.

NRR1 refers to citizens' deposits, which also applies to citizens' loans.

It couldn't be fairer - they would say at the fair in Benkovac.

NRR2 is obtained by calculating from the term funds of citizens increased by deposits of non-financial companies.

Tax changes through the magnifying glass

An average person's head is full of what was written and debated about tax changes, so we will take this opportunity to list the most important.

The decree on the minimum wage for 2024 established the minimum wage at 840 euros, while last year it was 700 euros.

Thus, the net amount of the minimum wage is around 677 euros this year.

Another question is who will pay for it, but not everything can... The legislator made it possible; it is up to the employer to pay.

There is no more income tax, but depending on the city or municipality of residence, it is possible to pay more tax - lower income tax rates can range from 15 to a maximum of 23.6%, and higher income tax rates from 25 to 35.4%.

The annual income tax at the lower rate will be settled on the tax base up to EUR 54,400, and at the higher tax rate above that amount - until now, the limit was EUR 47,780.28.

The city or municipal council lost tax revenue, but that's why they can now cut a more significant amount of tax on summer homes from 60 cents to 5 euros per m2. In contrast, the previous maximum amount was 2 euros.

The tax rate on income from property earned from rent and lease also increased - instead of a 10% + surtax rate, a single rate of 12% is now applied.

In the case of income from the alienation of real estate and real estate rights, the income tax is raised from the current 20 to 24 percent.

From this year, the personal deduction increases from 530.90 to 560 euros.

The coefficients used in calculating the increased personal deduction based on dependent members and disability are changing - from EUR 280 for the 1st child to EUR 2,744 for the 9th child, and for disability to EUR 168, and for total disability to EUR 560.

Tips will finally be able to be left via cards, whereby the tax-free tip amount - paid both in cash and via cards in the annual amount - will go up to 3,360 euros.

However, the law did not specify that those who earned the tip have the final say in the decision. Still, the amount they will see depends on the employer's goodwill.

The employer will have to declare the monthly amount of the collected tip according to the employee's OIB using the JOPPD form.

By amending the Rulebook on income tax, employers can pay larger amounts of tax-free receipts to workers, and here is an excerpt:

- Bonus amount - such as the Christmas bonus and annual vacation allowance - increases from 663.62 to 700 euros.

- Compensation for food costs for workers goes up by 403.56 euros - from a maximum of 796.44 euros to 1,200 euros.

- The award for work results increases from EUR 995.43 to EUR 1,120, which is a jump of EUR 124.57.

- The fee for using a private car for official purposes increases from 0.40 to 0.50 euros per kilometre travelled.

- Per diems for business trips in the country will be tax-free up to 30 euros, compared to the current 26.55 euros.

- The non-taxable amount of the employee's severance pay upon retirement will increase from the current maximum of 1,327.24 euros to 1,400 euros.

The inclusion of pupils and students in the labour market is stimulated - the amount of annual tax-free receipts for work through the pupil and student associations increases to 3,360 euros from the current 3,185.38 euros.

Creative space also opens up with scholarships for both students and athletes.

Namely, the non-taxable amount for scholarships increases from 232.27 to 560 euros per month, and for scholarships for excellent achievements, from 530.90 to 840 euros per month.

Tax-free amounts for sportsmen's scholarships will increase from 232.27 to 560 euros per month, and the tax-free amount of awards for sports achievements will increase from 2,654.48 euros to 2,800 euros.

Ivica Žuro

Ivica Žuro is a consultant in finance, banking and corporate management. He is the owner of MM Beneficium business consultancy. After a long career in banking where, among other things, he was a long-term director for Central Dalmatia at Splitska banka, he decided to use his experience in financing and management consulting. His specialism is the financing of entrepreneurship and legal persons, as well as the refinancing of existing obligations with more favourable lending, as well as organizational improvements and savings on business costs.

Categories of trends

- News

- Sale

- Marketing

- SEO

- Web design

- Social media

- Technology

- Regulations

- Management

- Education

- Finances

- User experience

- Graphic design

Newsletter

Sign up for the newsletter and receive the latest trends and tips straight to your inbox